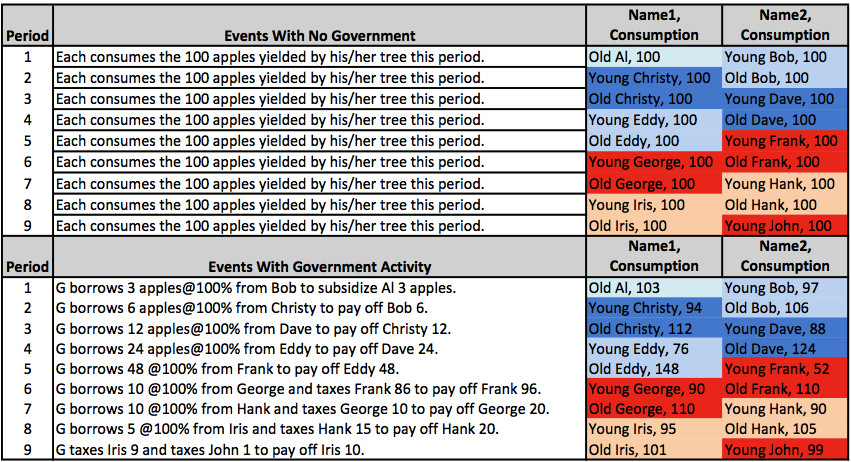

The spreadsheet is based on Bob Murphy's initial table, albeit with some slight changes. Perhaps most importantly, I assume that old people may now earn less than young people (where the Old:Young income ratio is determined by the parameter "a"). And we can obviously vary all other parameters as desired.

As we can see, it is ultimately the combination of variables and parameters -- say nothing of the assumptions used within this simple model -- that determine whether people are better off as a result of deficit financing and transfers. E.g. All else equal, a lower "a" will mean that government is able to transfer more from Old Al to Young Bob in the first period (i.e. higher "t"), whilst not lowering the utilities of future generations. Indeed, "t" is the most interesting parameter from my perspective since this is the one that Government must decide on when all the others are given exogenously.

For a more specific example, plug in the following values: r = 100%, g = 500%, a = 0.5 and t = 3. Clearly these large growth rates are absurd, but they serve to illustrate how subsequent generations can actually suffer a relative loss in utility if GDP growth ("g") is significantly higher than the interest rate ("r"). As I explained in my previous post, this is because I am assuming a diminishing marginal utility (DMU) function. However, you can offset things by now plugging in a = 0.2. This gives you an idea of how important the interplay between our parameters is.

I'd obviously encourage you to play around with things and see how your results change. As an added bonus, I've included a formula (in the light blue cell) that works out the maximum transfer for maintaining a neutral effect on utility, when we assume that utility is logarithmic.[*]

Please feel free to share and adapt as you wish. Of course, a pointer towards the original source would not go amiss.

THOUGHT FOR THE DAY: Relative to the non-intervention case, government deficits may or may not have negative consequences for the utilities of future generations... Like everything else in life, it depends on our starting assumptions. I sense that this might not be the definitive answer that some of you were hoping for, but so be it. That said, I'd suggest that plausible values for our parameters would be r = g = 3% and a = 0.75. In this case, one notes that government in our simple model could actually improve utilities quite easily by using deficit finance. (In the logarithmic utility case, they can transfer anything up to 25 units and still yield an improvement in the utility levels of future generations.)

___

[*] The formula is based on equating the laissez faire and deficit utilities:

ln(X) + ln(aX) = ln(X - t) + ln[(1 + g)aX + (1 + r)]

Taking exponents and a bit of algebra allows us to solve for t:

t = [1/(1 +r)] * X [(1 +r) - a(1 + g)]